Welcome to the future of trading, where data, speed, and precision replace guesswork and emotional decisions. Algorithmic trading, once the exclusive domain of institutional giants, is now more accessible than ever, especially for traders using powerful platforms like TradingView. The key to success, however, isn't just about having the right tools; it’s about deploying effective strategies for algo trading. This guide demystifies this powerful approach, breaking down complex concepts into simple, actionable steps. We will explore nine distinct strategies, giving you a clear roadmap to automate and enhance your market analysis.

This in-depth roundup moves beyond theory to provide practical, real-world applications. You will learn the core logic, primary benefits, and potential risks associated with each method, from foundational approaches like Mean Reversion and Momentum Trading to more advanced techniques involving statistical arbitrage and machine learning. We will cover:

This listicle is designed to be a comprehensive resource, providing the foundational knowledge you need to identify and implement the right strategy for your trading style. Whether you are a technical analyst seeking to automate support and resistance detection or a crypto trader needing AI-driven reversal signals, understanding these frameworks is the first step. For those looking to streamline the implementation process, integrated tools can translate these sophisticated strategies into clear, real-time alerts and signals directly on your charts, helping you trade with institutional-level insight without complex coding.

Mean reversion is one of the most foundational strategies for algo trading, built on a simple statistical principle: asset prices and historical returns eventually revert to their long-term average or mean. This approach operates like a stretched rubber band. The further a price moves away from its average, the stronger the potential force pulling it back. An algorithm identifies these extreme deviations and executes trades in the opposite direction, betting on this corrective snap-back.

This strategy thrives in markets that are range-bound or oscillating, rather than those in a strong, persistent trend. Its core logic is to "buy low" when an asset is oversold relative to its mean and "sell high" when it becomes overbought. Prominent quantitative hedge funds like Renaissance Technologies and Two Sigma have famously integrated sophisticated mean reversion models into their highly successful systematic strategies.

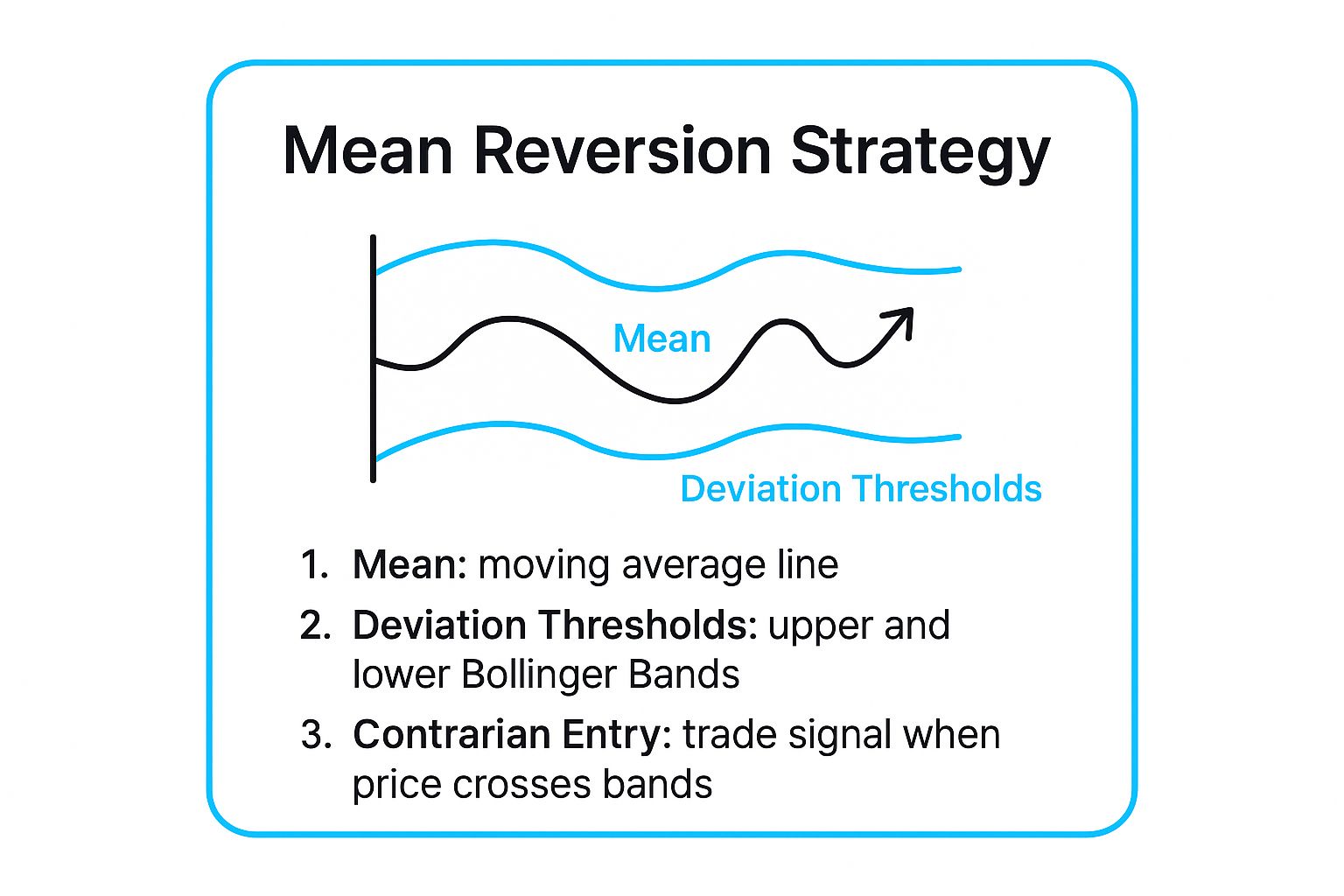

For TradingView users, implementing a mean reversion strategy often involves using technical indicators that measure deviation from a central value. The most common tools for this are Bollinger Bands and the Relative Strength Index (RSI).

Key Insight: The effectiveness of a mean reversion strategy hinges on accurately defining the "mean" and the "significant deviation." These parameters must be calibrated to the specific asset and market conditions, as a one-size-fits-all approach often fails.

The following infographic illustrates the core components of a mean reversion system using Bollinger Bands.

This visual shows how a contrarian entry is triggered when the price crosses the deviation thresholds, anticipating a return toward the central moving average. By combining these indicators within a Pine Script algorithm on TradingView, you can automate the process of identifying these setups and executing trades.

In direct contrast to mean reversion, the momentum trading strategy is built on the idea that "the trend is your friend." This is one of the most popular strategies for algo trading, operating on the principle that assets demonstrating strong upward or downward price movement will continue in that direction for a certain period. An algorithm designed for momentum trading identifies assets with strong directional conviction and executes trades to ride the wave, buying assets in an uptrend and shorting those in a downtrend.

This approach excels in markets experiencing clear, sustained trends and is less effective in choppy, range-bound conditions. Its core logic is to capitalize on the persistence of market sentiment, often fueled by news, earnings reports, or macroeconomic shifts. Pioneering firms like AQR Capital Management and the Winton Group have built incredibly successful quantitative funds around sophisticated trend-following and momentum models.

For TradingView users, building a momentum algorithm involves using indicators that measure the strength and direction of a trend. The Moving Average Convergence Divergence (MACD) and the Average Directional Index (ADX) are primary tools for this purpose.

Key Insight: The greatest challenge in momentum trading is distinguishing a genuine, sustainable trend from a short-lived breakout or "head fake." Successful algorithms often use a confluence of multiple indicators and strict risk management, like trailing stops, to protect profits and cut losses quickly when momentum fades.

By programming these indicators into a Pine Script algorithm, a trader can automate the detection of strong trends and execute entries with precision. This automates the process of catching significant market moves while they are still in progress.

Arbitrage is one of the oldest and theoretically risk-free strategies for algo trading, focusing on exploiting price discrepancies of an identical asset across different markets. The core principle is to simultaneously buy an asset where it's cheaper and sell it where it's more expensive, locking in the price difference as profit. Since these opportunities are often minuscule and exist for mere milliseconds, high-frequency trading (HFT) algorithms are essential to capitalize on them.

This strategy's success depends almost entirely on speed and efficiency rather than predicting market direction. Leading quantitative firms like Citadel Securities and Virtu Financial have built empires on sophisticated arbitrage systems that can execute millions of trades per day. For instance, a crypto arbitrage bot might buy Bitcoin on Exchange A for $60,000 and simultaneously sell it on Exchange B for $60,050, capturing a $50 profit per coin before fees.

While true HFT arbitrage is dominated by institutions, retail algo traders can implement simpler forms, especially in less efficient markets like cryptocurrency. Success requires a focus on speed, connectivity, and cost management.

Key Insight: The profitability of arbitrage is a race to zero. As more participants compete, price discrepancies shrink. Your competitive edge lies in minimizing latency and transaction costs, as these factors can easily erase the small profits generated from each trade.

Executing this strategy on TradingView is challenging due to platform limitations on multi-exchange execution. Traders typically build custom scripts using languages like Python, connecting directly to exchange APIs to monitor order books and execute trades with the lowest possible delay. This direct connection is paramount for any chance of success.

Market making is a sophisticated approach to algorithmic trading where the primary goal is to provide liquidity to the market rather than predicting price direction. A market making algorithm simultaneously places both a buy (bid) order and a sell (ask) order for an asset, profiting from the difference between them, known as the bid-ask spread. This strategy is the digital equivalent of a traditional market maker standing on a trading floor, ready to buy from sellers and sell to buyers at any moment.

This is one of the most high-frequency strategies for algo trading, requiring robust technology and low-latency connections. The algorithm constantly adjusts its bid and ask prices in response to market activity, aiming to capture the spread on a high volume of transactions while managing the risk of holding an unbalanced inventory. Giants in the financial world, such as Citadel Securities and Virtu Financial, have built their empires on advanced, large-scale market making operations across global markets.

For retail traders on platforms like TradingView, a simplified market making strategy can be built by focusing on a single asset and managing risk carefully. The core idea is to maintain a presence on both sides of the order book around the current market price.

Key Insight: Successful market making is less about predicting market direction and more about managing risk and probability. The biggest challenge is "adverse selection," where your orders get filled right before the price moves against you. Mitigating this risk is crucial for long-term profitability.

Your algorithm must be able to cancel and replace orders in milliseconds to react to market microstructure changes. By automating this process with a Pine Script bot connected to an exchange, you can systematically provide liquidity and aim to capture the spread, even in highly competitive markets.

Statistical Arbitrage, often called StatArb, is one of the more mathematically intensive strategies for algo trading. It moves beyond single-asset analysis to exploit temporary pricing inefficiencies between a pair or a basket of related securities. The core idea is that assets with a strong historical correlation will eventually revert to that relationship after a temporary divergence. An algorithm identifies these divergences, simultaneously buying the underperforming asset and shorting the outperforming one.

This strategy is inherently market-neutral, meaning its profitability depends on the relative performance of the assets within the basket, not the overall direction of the market. This makes it attractive for managing risk during volatile periods. Pioneering quantitative firms like Renaissance Technologies and D.E. Shaw built their empires on sophisticated versions of StatArb, using complex models to trade thousands of stocks based on these subtle mathematical relationships.

Implementing StatArb on TradingView involves identifying correlated assets and quantifying their relationship. While a full-scale pairs trading system requires advanced scripting, the foundational analysis can be done using built-in tools. A common approach is pairs trading, a simplified form of StatArb.

KO/PEP). This ratio will often oscillate around a historical mean. When the ratio deviates significantly from its mean, it signals a trading opportunity. You can apply indicators like Bollinger Bands to this ratio chart to identify entry and exit points.Key Insight: The success of a StatArb strategy rests on the stability of the statistical relationship (cointegration) between assets. Correlations can and do break down, especially during market stress. Constant model monitoring and recalibration are non-negotiable for long-term viability.

A StatArb algorithm automates this process by calculating the spread or ratio, identifying statistically significant deviations, and executing the long/short trades simultaneously. This requires robust backtesting to validate the pair's relationship across different market regimes before deploying capital.

High-Frequency Trading (HFT) is among the most technologically advanced strategies for algo trading, defined by its incredible speed and massive volume. These algorithms execute thousands or even millions of orders in fractions of a second, aiming to profit from minute price discrepancies and market inefficiencies that are invisible to human traders. The core principle is not large gains per trade, but minuscule profits earned consistently across an enormous number of trades.

This strategy is the domain of sophisticated quantitative firms like Citadel Securities and Virtu Financial, which invest heavily in co-location services (placing their servers in the same data centers as the exchange's servers) to minimize latency. HFT dominates modern markets, accounting for a significant portion of daily trading volume in equities and futures. Due to its extreme infrastructure and capital requirements, it is generally inaccessible to retail traders using platforms like TradingView.

While direct HFT implementation is beyond retail scope, understanding its concepts can inform faster-paced algorithmic approaches. HFT firms deploy various substrategies, but they often revolve around two key ideas: market making and arbitrage.

Key Insight: The success of HFT is a game of nanoseconds. It relies almost entirely on having a technological speed advantage and sophisticated infrastructure. Without co-location and direct market access, competing in this space is virtually impossible.

The image above visualizes the concept of an HFT firm's direct, ultra-low-latency connection to a financial exchange, bypassing slower, conventional internet routes. This physical proximity is what gives HFT its critical edge, allowing it to see market data and place orders faster than any other market participant. While you cannot replicate this on TradingView, the principle of minimizing latency remains relevant for any automated strategy.

A news-based trading strategy leverages technology to automatically interpret and act on market-moving information in real-time. This is one of the more advanced strategies for algo trading, as it moves beyond price data to analyze unstructured information from news articles, press releases, social media, and regulatory filings. Using techniques like Natural Language Processing (NLP) and sentiment analysis, an algorithm can gauge the tone of a news item (positive, negative, or neutral) and its potential market impact, executing trades within milliseconds of the information becoming public.

This approach is designed to capture the explosive volatility that often follows major announcements, such as earnings reports, central bank decisions, or unexpected geopolitical events. The core principle is that financial markets are inefficient in the short term and react predictably to certain types of news. Quantitative firms like Renaissance Technologies and data providers such as Ravenpack have built sophisticated systems to systematically exploit these reactions before human traders can fully process the information.

While building a proprietary NLP engine is complex, retail traders can access this strategy through specialized APIs and data feeds that provide structured news and sentiment data. The algorithm's logic is then built around these data points.

Key Insight: The greatest challenge in news-based trading is distinguishing genuine, market-moving information from noise and "fake news." A robust strategy requires multiple credible sources for verification and filters that can identify keywords associated with reliable announcements versus speculative rumors.

Successfully trading on news events requires a deep understanding of market catalysts and a disciplined, automated approach. For traders interested in this area, you can learn more about how to trade news events and earnings announcements on ezalgo.ai. By setting up a system that can parse and react to information faster than the broader market, you can find a significant edge.

Machine learning represents a frontier in strategies for algo trading, moving beyond fixed rules to create systems that can learn and adapt. Instead of programming explicit "if-then" conditions, a machine learning strategy uses algorithms to analyze vast datasets, identify complex patterns, and make predictive trading decisions. These models can continuously refine their approach as new market data becomes available, evolving to changing conditions.

This sophisticated approach is the powerhouse behind some of the world's most successful quantitative funds, including Renaissance Technologies and Two Sigma. Their models sift through historical price data, alternative datasets like satellite imagery or social media sentiment, and economic reports to find predictive signals that are invisible to the human eye. The goal is to build a system that doesn't just follow rules but discovers its own for generating alpha.

Implementing a machine learning model for trading is an advanced process that hinges on data science principles. It involves training models like Support Vector Machines (SVM), Random Forests, or Neural Networks to predict future price movements based on historical inputs, known as "features."

Key Insight: The success of a machine learning strategy depends less on the complexity of the algorithm and more on the quality of the data and the creativity of the feature engineering. A simple model with excellent features will almost always outperform a complex model with poor features.

Properly validating these models is non-negotiable, requiring rigorous testing on data the model has never seen before. You can find out more about the importance of robust validation in our guide on how to backtest a trading strategy. By using out-of-sample and forward testing, you can gain confidence that your model has genuine predictive power and isn't just a product of overfitting.

Grid trading is a systematic method that profits from market volatility by placing a series of buy and sell orders at predefined intervals around a set price. This network of orders creates a "grid." As the price fluctuates within this range, the algorithm automatically executes "buy low" orders as the price falls and "sell high" orders as it rises, capturing small profits from each completed pair of trades. This is one of the more methodical strategies for algo trading, designed to perform well in sideways or ranging markets where price action is choppy but contained.

The strategy excels in markets that lack a clear directional trend, such as certain forex pairs or cryptocurrencies during periods of consolidation. Automated grid bots offered by platforms like Pionex and 3Commas have made this strategy highly accessible, allowing traders to deploy it with minimal manual intervention. The core appeal lies in its ability to generate consistent, small gains from natural market oscillations without needing to predict the market's next major move.

On TradingView, implementing a grid trading strategy involves scripting an algorithm that can manage multiple limit orders simultaneously. This requires careful planning of the grid's parameters: the upper and lower price boundaries, the number of grid levels, and the size of each order.

Key Insight: The greatest risk in grid trading is a strong, sustained trend that moves outside your predefined range. A well-placed stop-loss for the entire grid system is crucial to prevent significant drawdowns if the market breaks out decisively in one direction.

This systematic approach can be particularly effective for traders who want to capitalize on volatility without the stress of active market timing. By automating the placement and management of orders, grid trading offers a structured way to engage with ranging markets.

We have navigated through a diverse landscape of powerful strategies for algo trading, from the rhythmic ebb and flow of Mean Reversion to the adaptive intelligence of Machine Learning models. You’ve seen how momentum can be systematically captured, how statistical arbitrage finds hidden relationships between assets, and how even news events can be transformed into quantifiable trading signals. Each of these nine strategies offers a distinct lens through which to view and interact with the financial markets.

However, understanding the theory behind these concepts is just the starting point. The real journey begins with application. The path from a theoretical strategy to a live, executing algorithm is filled with challenges: coding complexity, rigorous backtesting, continuous optimization, and the ever-present need to manage risk effectively. This is where many aspiring algorithmic traders hit a wall, spending more time debugging code than analyzing market opportunities.

The critical takeaway is that successful algo trading isn’t just about having the best idea; it’s about having the most robust and efficient execution. Whether you are a retail trader looking for an edge, a technical analyst aiming for precision, or a crypto trader navigating volatile markets, the goal is the same: to turn a strategic plan into profitable action with consistency and discipline.

To do this effectively, you must focus on the following core pillars:

Key Insight: The most successful algorithmic traders are not necessarily the best programmers; they are the best systems thinkers who know how to leverage the right tools to execute a well-defined plan with unwavering discipline.

Embracing the world of algorithmic trading is a commitment to a more systematic, data-driven approach. It’s about replacing emotional impulses with calculated probabilities and gut feelings with backtested evidence. The strategies we've discussed are your blueprint. Now, you must choose your tools to build the structure.

You can choose the difficult path of building everything from scratch, which requires deep expertise in programming, data science, and infrastructure management. Or, you can choose a smarter path: leveraging a solution that has already done the heavy lifting. This allows you to stand on the shoulders of experts and focus your energy on what truly matters, refining your approach and managing your trades.

The evolution from a discretionary trader to a systematic one is one of the most significant leaps you can make. By mastering these strategies for algo trading, you are not just learning new techniques; you are fundamentally changing your relationship with the market. You are becoming the architect of your own trading system, equipped with the precision, speed, and objectivity needed to thrive in today’s competitive environment.

Ready to implement these advanced strategies without the steep learning curve of coding? The EzAlgo indicator suite for TradingView automates the complex analysis behind these concepts, delivering clear, actionable buy and sell signals directly to your chart. Stop guessing and start trading with a data-driven edge by visiting EzAlgo to see how our tools can elevate your performance.

%201.svg)